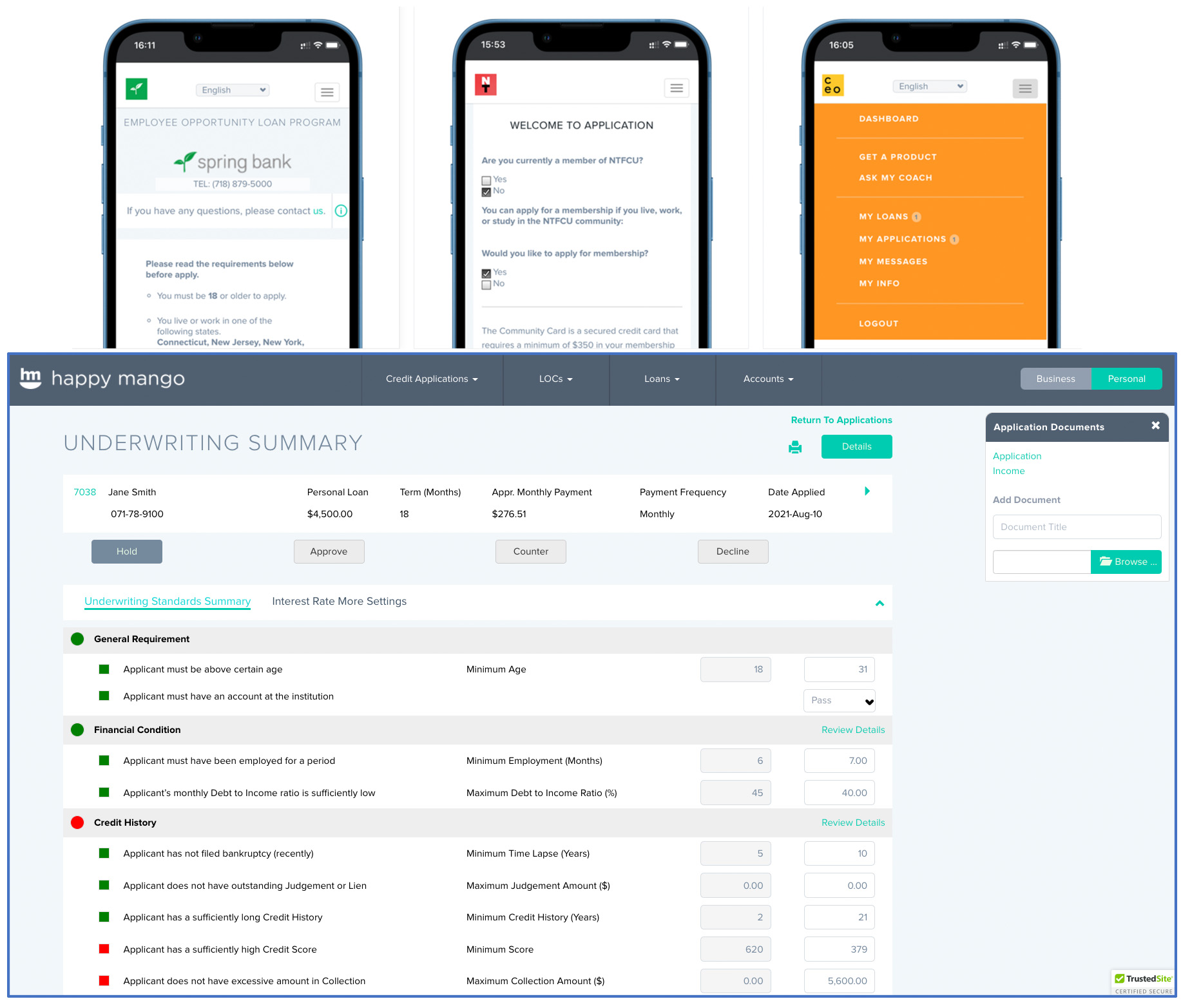

End-to-End Lending Solution

- Mobile Intake and Closing

- Consumer and Business Loans

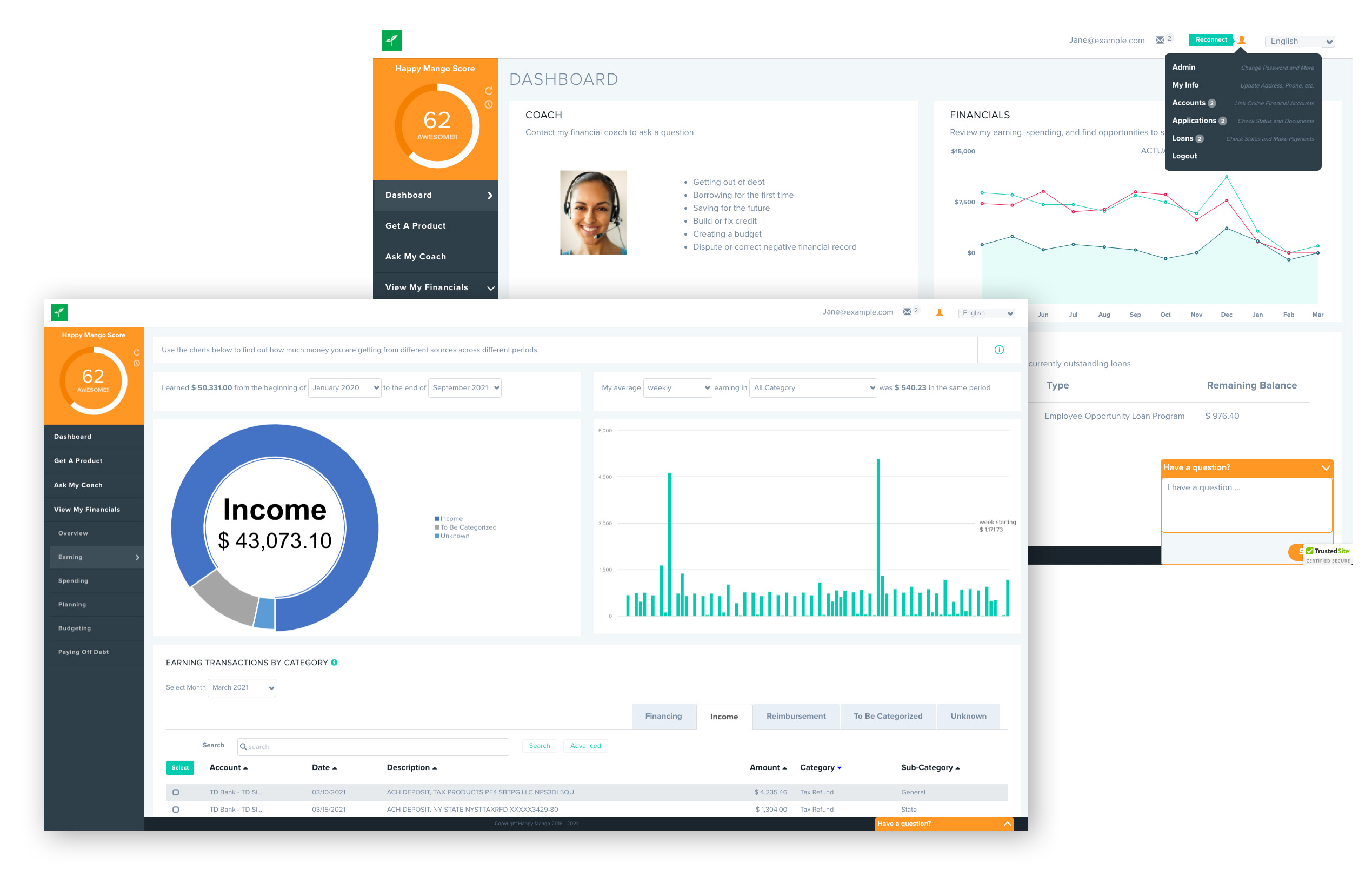

- Automated Financial Analysis

- Integrated Credit Reporting

- Same-Day ACH

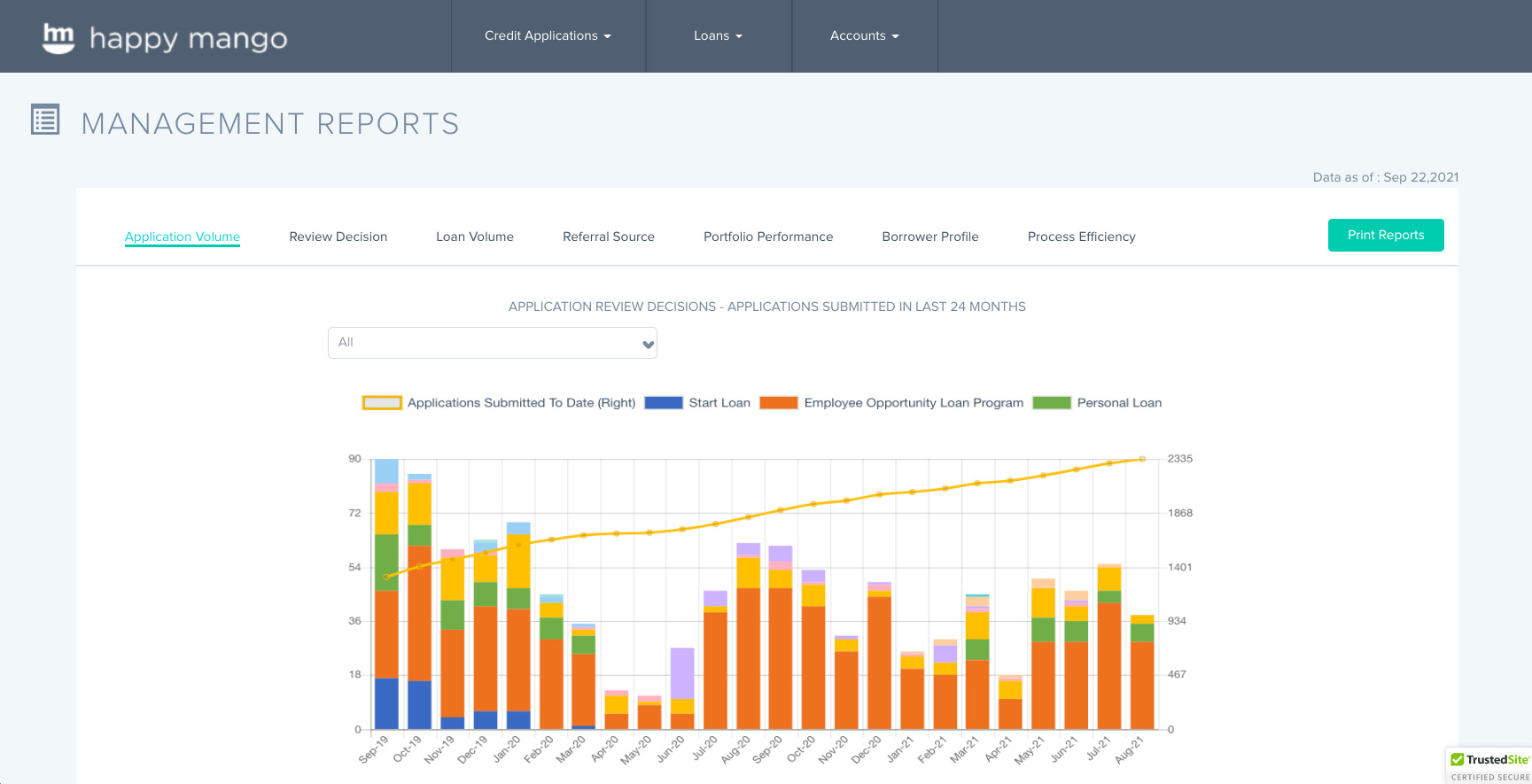

Impact and Growth Tool Box

- Referral Tracking

- Business Partnership

- Community Collaboration

- Online Marketing Tools

- Impact Analysis and Reporting